Last year, Lori Stacy, the CEO of Norfolk-based Trader Interactive, found herself amongst a select group of Virginia Unicorn Entrepreneurs after the company’s acquisition by Australian auto retailer carsales.com Ltd. Although the newfound public attention presented challenges, such as the poaching of scarce tech talent, Stacy acknowledged the morale boost for employees and the influx of cash for further investment as significant benefits. Virginia has proven to be a fertile ground for unicorn startups, with at least ten companies attaining unicorn status in recent years. In particular, artificial intelligence-driven kidney care startup Somatus, which recently achieved a valuation of $2.5 billion, and cybersecurity firm Expel Inc. have demonstrated the potential for substantial growth within the state’s supportive entrepreneurial ecosystem.

Introduction

From Virginia Business By GREG WEATHERFORD

The Unicorn

Last year, Lori Stacy found herself leading a unicorn.

The CEO of Norfolk-based Trader Interactive, an online marketplace for boats, recreational vehicles, motorcycles, and other niche vehicles, Stacy helped shepherd the company through its June acquisition by Australian auto retailer carsales.com Ltd.

Challenges and Bonuses

While nothing on the surface changed, Trader Interactive’s unicorn status did confer some bonuses — and challenges.

“Any time valuation is public; personally, I don’t love that,” Stacy says. For one thing, she says, the attention draws poachers of tech talent, already scarce in Hampton Roads.

Benefits of Unicorn Status

But she does allow that the status is great for morale. “Any time there’s a success, it brings confidence, and that’s great for our employees. They like to win and celebrate those wins,” Stacy says. “And a lot of our customers are excited.”

The influx of cash that valuation brought was nice, too, Stacy acknowledges. “It gives us investment opportunities to try new things to support our clients. When you’re struggling to grow, resources are more scarce,” she says. But after CarSales.com’s investment, there was “a lot more room for experimenting. So, it’s a win all around.”

Virginia’s Unicorns

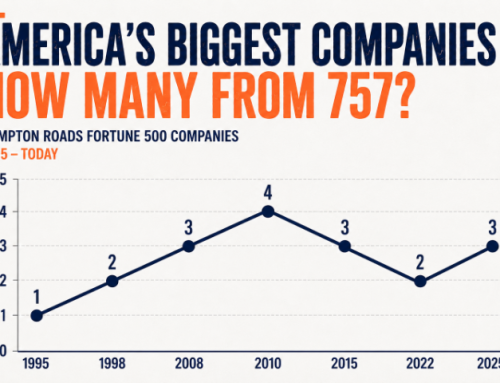

Virginia has its own stable of unicorns. According to international venture capital tracking firm Dealroom.co and other sources, at least 10 Virginia companies reached unicorn status in the last few years, though two went through IPOs last year and are now publicly traded. (See chart, Page 25.)

Virginia’s Advantage

Virginia offers a lot of advantages for startups to succeed, says Dr. Ikenna Okezie, the Harvard-educated co-founder and CEO of Somatus, an artificial intelligence-driven kidney care startup based in McLean that recently hit a valuation of $2.5 billion.

Trader Interactive’s Journey

Trader Interactive started as a publisher of modest newsprint booklets of ads for vehicles like RVs, motorcycles and boats. Its larger corporate sibling, Autotrader.com Inc., did the same for cars.

Expel Inc.: A Cybersecurity Unicorn

For Expel Inc., a cybersecurity firm based in Herndon, the problem to solve is less technical and more interpersonal.

Expel co-founder and Chief of Staff Yanek Korff says that when he and his partners launched the business in 2016, “we were more excited about building a … company from a culture perspective than a security perspective. You could say it was about the journey.”

Question & Answer

What is Trader Interactive?

Trader Interactive is an online marketplace based in Norfolk that deals with boats, recreational vehicles, motorcycles, and other niche vehicles.

What benefits did Lori Stacy mention about being a unicorn company?

Lori Stacy mentioned that being a unicorn company brought a morale boost for employees and an influx of cash for further investment opportunities.

How many companies in Virginia have reached unicorn status in recent years?

At least 10 companies in Virginia have reached unicorn status in the last few years according to international venture capital tracking firm Dealroom.co and other sources.